Navigating the complexities of a loved one's estate after their passing is undoubtedly challenging, and among the many financial considerations, understanding the fate of a mortgage often stands out. It's a question that brings forth a mix of legal intricacies, emotional weight, and practical steps. The immediate aftermath requires careful attention to detail, as lenders and beneficiaries alike must adhere to specific procedures and timelines to ensure a smooth transition and avoid potential complications.

Understanding the Initial Steps After a Borrower's Death

Upon the death of a mortgage borrower, the first crucial step is to notify the lender. This seemingly simple action initiates a series of processes that are dictated by both federal regulations and the terms of the mortgage agreement itself. Failing to inform the lender promptly can lead to misunderstandings or even unintended consequences for the estate and its heirs.

The executor of the estate, or a designated representative, typically takes on the responsibility of contacting the mortgage servicer. This notification should include proof of death, such as a death certificate, and information about the executor or administrator appointed to manage the estate. This initial communication sets the stage for how the mortgage will be handled moving forward.

The Role of the Estate and Probate

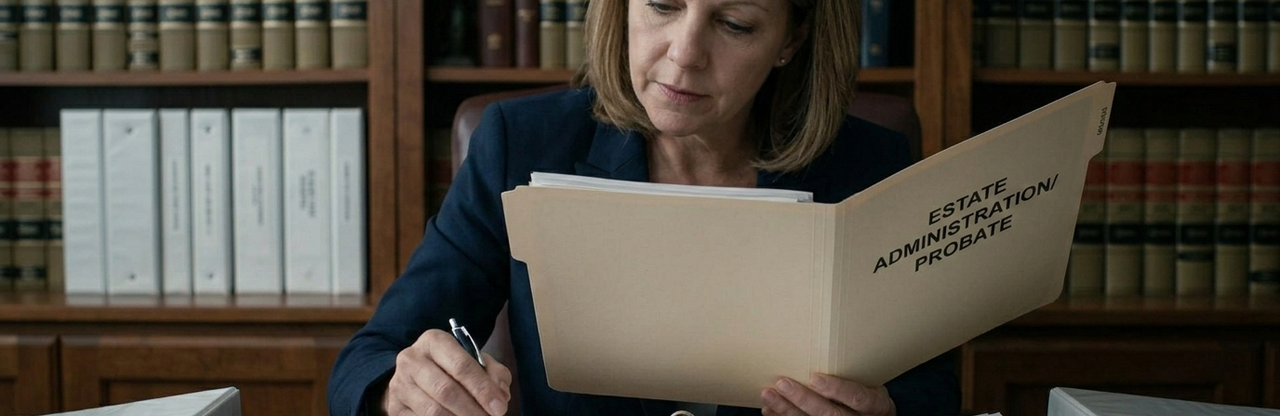

When a borrower dies, their assets and liabilities, including the mortgage, become part of their estate. This estate typically goes through a legal process known as probate, especially if there's a will. During probate, the will is validated, assets are inventoried, and debts are settled before remaining assets are distributed to beneficiaries.

The estate's job is to manage the deceased's financial obligations, including mortgage payments, until a more permanent solution can be arranged. This might involve continuing payments from estate funds or identifying a new owner for the property. The probate court oversees this entire process, ensuring legal compliance.

Successor in Interest: Who Can Take Over the Mortgage?

A critical concept in this scenario is the "successor in interest." This refers to an individual who inherits the property and, under federal law (specifically the Garn-St. Germain Depository Institutions Act of 1982), has the right to assume the existing mortgage terms. This act protects family members from automatic foreclosure when a borrower dies.

Common successors in interest include spouses, children, or other relatives who were living in the home at the time of the borrower's death. Lenders cannot demand immediate repayment or accelerate the loan solely because of the borrower's passing if a qualified successor in interest is identified.

Options for Managing the Mortgage

There are several pathways for dealing with a mortgage after the original borrower passes away. The most common options include assuming the loan, selling the property, or allowing the property to go into foreclosure. Each option carries its own set of legal and financial implications for the estate and potential heirs.

The choice often depends on the financial capacity of the heirs, their desire to keep the property, and the overall value of the estate. Careful consideration and professional advice are essential before making any major decisions regarding the property and its associated debt.

Assumption of the Mortgage

One of the most straightforward options for a successor in interest is to assume the existing mortgage. This means they take over the responsibility for making the payments under the original loan terms, including the interest rate and remaining balance. The lender must generally allow this assumption for qualified successors.

To assume the mortgage, the successor in interest will need to formally notify the lender and provide necessary documentation. While the lender cannot require a credit check for a qualified successor, they may ask for information to confirm identity and relationship to the deceased borrower.

Selling the Property to Pay Off the Mortgage

If no one wishes to assume the mortgage or is financially able to, selling the property is a common solution. The proceeds from the sale are then used to pay off the outstanding mortgage balance. Any remaining funds become part of the estate and are distributed according to the will or state law.

This option can be particularly appealing if the property has significant equity, providing a way to settle the debt without placing a financial burden on heirs. The executor of the estate typically manages the sale process, ensuring all legal and financial obligations are met.

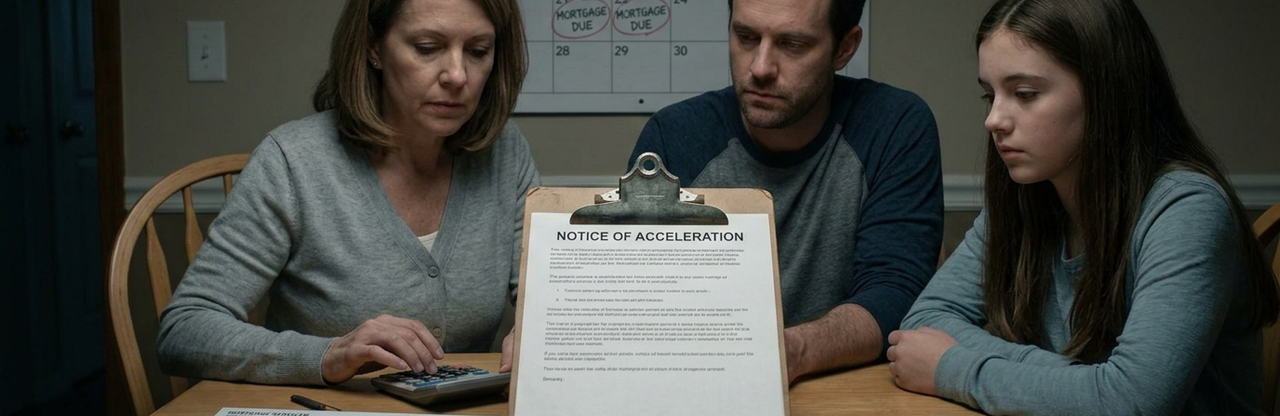

Foreclosure and Its Implications

In unfortunate circumstances, if no one assumes the mortgage and the property cannot be sold to cover the debt, the property may face foreclosure. This happens when mortgage payments cease and the lender exercises their right to reclaim the property to recover their losses. Foreclosure is generally a last resort.

It's crucial for the estate or heirs to communicate with the lender if they anticipate difficulties in making payments or managing the property. Lenders often have programs or options available to prevent foreclosure, especially when dealing with the death of a borrower.

Special Considerations for Reverse Mortgages

Reverse mortgages operate differently from traditional mortgages, and their handling after a borrower's death also differs significantly. With a reverse mortgage, the loan typically becomes due and payable when the last borrower dies or permanently leaves the home.

Heirs usually have a set period, often six months, to either repay the loan balance, sell the home, or refinance it. If the home's value is less than the loan balance, heirs are generally not personally responsible for the shortfall, as reverse mortgages are non-recourse loans.

Estate Planning and Digital Assets

While focusing on the mortgage, it's also vital to consider the broader scope of estate planning, especially in today's digital age. Many financial accounts, communications, and important documents are now online, making access challenging after a death. This can indirectly impact how a mortgage is managed, as critical information might be stored digitally.

Ensuring that digital assets are accounted for in estate planning can significantly streamline the process of managing financial affairs, including mortgages, post-mortem. For those seeking comprehensive solutions for managing their digital legacy, Cipherwill offers a robust platform designed to help individuals plan and organize their digital estate. This can be invaluable in ensuring that crucial information, such as mortgage details or contact information for lenders, is accessible to the right people at the right time.

Preventing Future Complications: Best Practices

Proactive estate planning is the most effective way to prevent complications regarding a mortgage after a borrower's death. This involves clear communication, proper documentation, and sometimes specific legal arrangements. Taking these steps can provide peace of mind for both the borrower and their loved ones.

- Create a detailed will: Clearly state who inherits the property and how debts should be handled.

- Maintain accessible records: Keep mortgage documents, lender contact information, and account details in a secure, accessible place that an executor can find.

- Communicate with beneficiaries: Discuss your wishes and financial arrangements with those who will be responsible for your estate.

- Consider life insurance: A life insurance policy can provide funds to pay off the mortgage, relieving financial burden on heirs.

- Add co-borrowers or co-owners: If appropriate, adding another responsible party to the mortgage or deed can simplify transitions.

When planning for your digital assets and ensuring that your wishes are clearly understood by your loved ones, exploring resources like the Cipherwill blog can be incredibly beneficial. For more insights into how courts handle digital wishes and how families can prepare, you might find this post helpful: How Courts Handle Digital Wishes: A Simple Family Guide.

Key Takeaways for Heirs and Executors

For heirs and executors, understanding these processes is paramount. The immediate aftermath of a borrower's death is a sensitive time, and having a clear roadmap for managing the mortgage can alleviate significant stress. Prompt action, clear communication with lenders, and seeking professional advice are all crucial.

Remember that federal law provides protections for successors in interest, ensuring that lenders cannot automatically demand repayment. However, these protections require the successor to actively engage with the lender and follow the proper procedures to assume the loan or explore other options.

Conclusion

The death of a borrower introduces a complex set of procedures for handling a mortgage. From notifying the lender and navigating probate to understanding successor in interest rights and exploring options like assumption or sale, each step requires careful attention. Proactive estate planning and leveraging digital estate management tools can significantly simplify this difficult process, ensuring a smoother transition for all involved.

Frequently Asked Questions

Q: What is the first thing I should do about the mortgage after a loved one dies?

A: The very first step is to notify the mortgage lender or servicer as soon as possible. You'll typically need to provide a death certificate and information about the executor or administrator of the estate.

Q: Can the bank immediately foreclose on the house after the borrower dies?

A: No, federal law, specifically the Garn-St. Germain Act, generally prevents lenders from immediately foreclosing or demanding full repayment solely because of the borrower's death, especially if there's a qualified successor in interest.

Q: Who is considered a "successor in interest" for a mortgage?

A: A successor in interest is typically someone who inherits the property and can assume the mortgage. This often includes spouses, children, or other relatives who lived in the home at the time of the borrower's death.

Q: Do I need to re-qualify for the mortgage if I am a successor in interest?

A: Generally, no. If you are a qualified successor in interest, the lender cannot require you to undergo a credit check or re-qualify for the loan. You simply assume the existing terms.

Q: What if I don't want to keep the house or can't afford the mortgage payments?

A: You have options. You can sell the property to pay off the mortgage, or if the estate cannot manage the debt, the property might eventually go into foreclosure. It's best to communicate openly with the lender about your situation.

Q: Will the deceased borrower's debt transfer to me if I inherit the house?

A: The mortgage debt itself is tied to the property, not personally to the heir, unless you formally assume the loan. If you don't assume the loan, you aren't personally liable for the debt beyond the value of the inherited property.

Q: How does a reverse mortgage differ when the borrower dies?

A: For a reverse mortgage, the loan generally becomes due and payable when the last borrower dies or permanently moves out. Heirs usually have a set period (e.g., six months) to repay the loan, sell the home, or refinance it.

Q: What if the house is worth less than the mortgage balance?

A: If it's a traditional mortgage, the estate is still responsible for the full balance. If it's a reverse mortgage, heirs are typically protected by the non-recourse nature of the loan, meaning they usually won't owe more than the home's value or 95% of its appraised value.

Q: Should I continue making mortgage payments after the borrower dies?

A: Yes, it's generally advisable to continue making payments if possible, either from estate funds or personally, to avoid late fees, damage to credit (if you're a co-borrower), or potential foreclosure actions while the estate is being settled.

Q: How can estate planning help with mortgage issues after death?

A: Comprehensive estate planning, including a will and clear instructions for digital assets, ensures that your wishes are known, and critical financial information (like mortgage details) is accessible. This significantly streamlines the process for your loved ones and helps prevent complications.