When a loved one passes away, the emotional toll is immense, and navigating the practicalities of their estate can add significant stress. Among the many financial considerations, understanding what happens to outstanding debts, particularly car loans, is a common concern. This situation can be complex, involving legal principles, financial institutions, and the specifics of the deceased's estate plan. It's crucial for family members to approach this with clarity and a structured understanding of the potential outcomes.

The immediate aftermath of a death often leaves family members grappling with grief, making it difficult to focus on administrative tasks. However, addressing financial obligations promptly can prevent further complications down the line. Car loans, unlike some other debts, are often tied to a physical asset, which introduces unique challenges and options for resolution. The specific terms of the loan agreement and the state's probate laws will heavily influence the path forward.

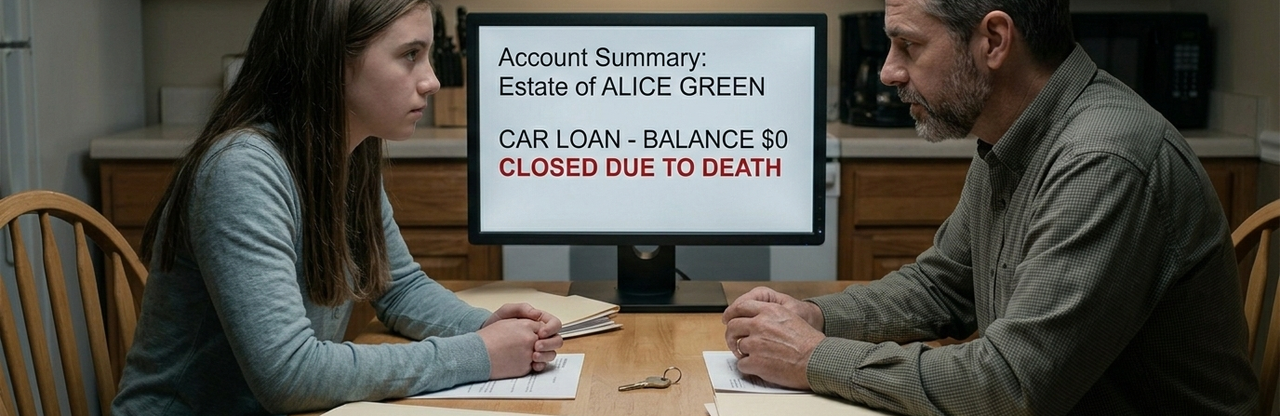

The Estate's Role in Debt Repayment

Upon an individual's death, their assets and liabilities collectively form their estate. This estate is then typically managed by an executor or administrator, whose responsibility it is to settle debts and distribute remaining assets according to the will or state law. A car loan is considered a debt of the estate, meaning the estate's assets are primarily responsible for its repayment. This fundamental principle guides much of the subsequent action.

It's important to understand that family members are generally not personally liable for the deceased's debts unless they were a co-signer or joint account holder. The estate acts as a separate legal entity for these purposes. Creditors, including the car loan lender, will file claims against the estate to recover what they are owed.

Secured vs. Unsecured Debts

Car loans fall under the category of secured debt. This means the loan is backed by collateral – in this case, the vehicle itself. This distinction is critical because it gives the lender specific rights that they wouldn't have with an unsecured debt like a credit card. If the loan isn't repaid, the lender has the legal right to repossess the collateral.

Unsecured debts, conversely, are not tied to any specific asset. While they are still claims against the estate, the lender's recourse is generally limited to the estate's general assets. The secured nature of a car loan often prioritizes its repayment from the estate's funds or requires specific actions regarding the vehicle.

Who is Responsible for the Loan?

The primary responsibility for a car loan after the borrower's death falls to their estate. The executor or administrator of the estate will be tasked with identifying all debts, including the car loan, and determining how they will be paid. This process often involves notifying creditors of the death and initiating communications regarding outstanding balances.

If the deceased had a co-signer on the car loan, that individual becomes fully responsible for the entire remaining balance. A co-signer legally agreed to be equally liable for the debt from the outset. Similarly, if the loan was a joint loan, the surviving joint borrower assumes full responsibility.

Options for the Estate and Family

Several pathways exist for resolving a car loan after the borrower's death, depending on various factors. One common option is for the estate to simply continue making payments until the loan is paid off, especially if a beneficiary wishes to keep the car. Another approach involves selling the vehicle and using the proceeds to satisfy the outstanding loan balance.

Alternatively, if the estate lacks sufficient funds or no one wishes to keep the car, the lender may repossess the vehicle. This is usually a last resort for lenders, as they prefer to have the loan repaid. Each option carries its own set of financial and logistical implications for the estate and surviving family.

The Role of Co-Signers and Joint Owners

As mentioned, co-signers and joint owners face immediate responsibility for the car loan upon the primary borrower's death. This is a crucial point often overlooked in estate planning discussions. A co-signer's credit can be negatively impacted if payments are missed, even if they were not the primary driver of the vehicle.

Joint ownership of the car itself further complicates matters. If the surviving joint owner is also a co-signer on the loan, their responsibility is clear. If they are a joint owner of the car but not on the loan, the situation can become entangled with estate liabilities, though they would still typically have a claim to the vehicle.

Impact of Life Insurance Policies

Some car loans are accompanied by credit life insurance policies. These policies are designed to pay off the outstanding loan balance in the event of the borrower's death. If such a policy exists, it can significantly simplify the process, as the insurance payout directly covers the debt, freeing the estate from this obligation.

It's essential for the executor or family members to investigate whether such a policy was in place. This information can usually be found in the original loan documents or by contacting the lender directly. A credit life insurance policy can provide immense relief during a difficult time.

Navigating Digital Assets and Estate Planning

In today's digital age, managing an estate extends beyond physical documents and financial statements. Many crucial pieces of information, including loan details, insurance policies, and communication records with lenders, might be stored digitally. Accessing these digital assets can be a significant hurdle for executors and family members. This is where comprehensive digital estate planning becomes invaluable.

Without proper planning, passwords, account information, and critical documents can be lost or inaccessible, causing delays and added stress. For those grappling with the complexities of managing a loved one’s digital footprint and ensuring all financial obligations, including car loans, are properly addressed, a robust solution is essential.

This is precisely where Cipherwill steps in as a comprehensive service solution. Cipherwill helps users organize and secure their digital assets, ensuring that loved ones can easily access vital information when needed. From financial accounts to social media profiles and important documents, Cipherwill provides a centralized, secure platform for digital estate planning, making the post-death administration process smoother and less overwhelming.

Repossession and Deficiency Balance

If the estate cannot or chooses not to pay off the car loan, and no co-signer steps forward, the lender has the right to repossess the vehicle. After repossession, the car is typically sold at auction. The proceeds from the sale are then applied to the outstanding loan balance.

If the sale price does not cover the entire loan amount, the remaining debt is known as a "deficiency balance." This deficiency balance still remains a debt of the estate. The lender can pursue the estate for this amount, which could impact other beneficiaries or assets within the estate.

Best Practices for Executors and Families

- Communicate with the Lender Immediately: Notify the car loan lender of the borrower's death as soon as possible. This opens lines of communication and allows you to understand their specific procedures and options.

- Locate All Loan Documents: Gather all relevant paperwork, including the original loan agreement, payment history, and any associated insurance policies. These documents contain crucial details about the loan terms.

- Assess Estate Finances: Determine the overall financial health of the estate. Can the estate afford to continue payments or pay off the loan? This assessment will guide your decision-making.

- Consult Legal Counsel: An estate attorney can provide invaluable guidance on navigating probate laws, creditor claims, and the best course of action for the estate.

- Consider Credit Life Insurance: Check if the deceased had credit life insurance on the car loan. This could resolve the debt entirely and prevent further financial burden.

- Evaluate Vehicle Value: If considering selling the car, get an accurate appraisal of its market value to understand if it will cover the outstanding loan.

Preventing Future Complications

Proactive estate planning is the most effective way to prevent complications regarding car loans and other debts after death. This includes clearly outlining wishes in a will, maintaining an organized record of financial accounts and debts, and discussing these arrangements with trusted family members or an executor.

For ongoing management of digital assets and important financial information, services like Cipherwill provide a structured approach. They help individuals organize their digital legacy, ensuring that crucial details, including those related to car loans and other financial obligations, are accessible to designated individuals when the time comes. This foresight can significantly reduce stress and burden on surviving family members.

Legal and State-Specific Considerations

The laws governing estates and debt repayment can vary significantly from state to state. Some states have "non-claim statutes," which set specific time limits within which creditors must file claims against an estate. Missing these deadlines can sometimes invalidate a creditor's claim.

Understanding the specific probate laws in the deceased's state of residence is vital. An estate attorney familiar with local regulations can offer tailored advice and ensure the estate complies with all legal requirements, protecting both the estate and the executor from potential liability.

Impact on Surviving Family Members' Credit

Generally, the death of a borrower does not directly impact the credit score of surviving family members, unless they were a co-signer or joint account holder. The deceased's credit report becomes inactive. However, if a family member was a co-signer and payments are missed, their credit will be severely affected.

Even for non-co-signers, if the estate is mishandled or debts are not properly addressed, it can lead to stressful and complicated situations. Ensuring the estate is settled efficiently and debts are managed appropriately is essential for everyone involved. For additional insights on financial responsibilities, especially after significant life changes, you might find this article helpful: After Graduation: The Responsibilities No One Mentions.

The Emotional and Practical Burden

Beyond the legal and financial aspects, the death of a loved one brings an immense emotional burden. Dealing with financial matters, especially a car loan, can feel overwhelming during this time. Having a clear understanding of the process and available options can provide some sense of control and alleviate additional stress.

Seeking support from legal professionals, financial advisors, and grief counselors can be beneficial. Preparing for these eventualities through thorough estate planning and utilizing digital asset management tools can soften the practical burden on grieving families, allowing them more space to heal.

Q&A

Q: Is a spouse automatically responsible for a deceased partner's car loan?

A: Not necessarily. A surviving spouse is only personally responsible if they were a co-signer on the loan or if they live in a community property state where specific rules apply to marital debt. Otherwise, the loan is a debt of the deceased's estate.

Q: What if the car is worth less than the outstanding loan balance?

A: If the car is sold and the proceeds don't cover the loan, the remaining amount is a "deficiency balance." This balance remains a debt of the estate, which the lender can pursue from other estate assets.

Q: Can the lender immediately repossess the car after someone dies?

A: Generally, no. Lenders must typically file a claim against the estate and follow probate procedures. They cannot usually just repossess the vehicle without notice, especially if payments are being made or arrangements are being discussed with the executor.

Q: What is credit life insurance and how does it help with a car loan?

A: Credit life insurance is a policy that pays off the outstanding balance of a loan if the borrower dies. If the deceased had such a policy on their car loan, the insurer would pay the lender, relieving the estate of that debt.

Q: Does having a will simplify the process for a car loan after death?

A: Yes, a will designates an executor who has the legal authority to manage the estate, including communicating with creditors and making decisions about assets like cars. This streamlines the process significantly compared to intestacy (dying without a will).

Q: Can I take over the car loan payments if I'm not a co-signer?

A: Potentially. You would need to contact the lender and discuss your options. They might allow you to assume the loan, or you might need to refinance it in your own name, depending on their policies and your creditworthiness.

Q: What happens if the estate has no money to pay the car loan?

A: If the estate is insolvent (has more debts than assets), the car loan lender may repossess the vehicle. If the sale of the car doesn't cover the loan, the lender may have to write off the remaining deficiency balance.

Q: How long does an executor have to deal with the car loan?

A: The timeline varies by state and the complexity of the estate. Executors should address debts promptly, often within the specific "non-claim" periods set by state probate laws, which can range from a few months to over a year.

Q: Will the car loan debt be reported on the deceased's credit report?

A: The deceased's credit report typically becomes inactive after their death. Any outstanding debts, including the car loan, are handled by the estate and generally do not affect the credit scores of surviving family members unless they were co-signers.

Q: What if the car was jointly owned but only one owner was on the loan?

A: If the car was jointly owned, the surviving joint owner would typically inherit ownership of the vehicle. However, the loan itself remains a debt of the deceased's estate. The surviving owner would need to work with the estate to decide whether to pay off the loan, assume it, or sell the car.