When a family member dies unexpectedly, the immediate barrier to their estate is no longer a heavy bank vault or a complex probate filing. It is a six-digit secure authentication code sent to an iPhone locked by a fingerprint they can no longer provide. Families who believe their digital estate planning is complete because they drafted a traditional paper will are walking into an operational nightmare. The physical death of an individual triggers a secondary crisis: the permanent cryptographic lockout of their digital assets, financial access points, and essential business infrastructure.

Preventing loved ones from being locked out of essential accounts requires understanding the severe limitations of legacy estate law when confronted by modern cybersecurity architecture.

The Anatomy of a Digital Lockout: Marcus's Architecture

Consider the reality of Marcus, a 42-year-old digital agency owner who managed his family’s finances, crypto investments, and corporate accounts. Marcus was thorough. He had a legally binding last will and testament drafted by a premium law firm, naming his wife, Sarah, as the sole beneficiary and executor. He even kept a secure spreadsheet on his primary laptop containing his bank routing numbers and account usernames.

When Marcus passed away suddenly, Sarah assumed the transition would be emotionally devastating but operationally straightforward. Following the advice of their probate attorney, she sat down to begin consolidating Marcus’s accounts. That was exactly when the modern security infrastructure—designed to protect Marcus from hackers—turned against his own family.

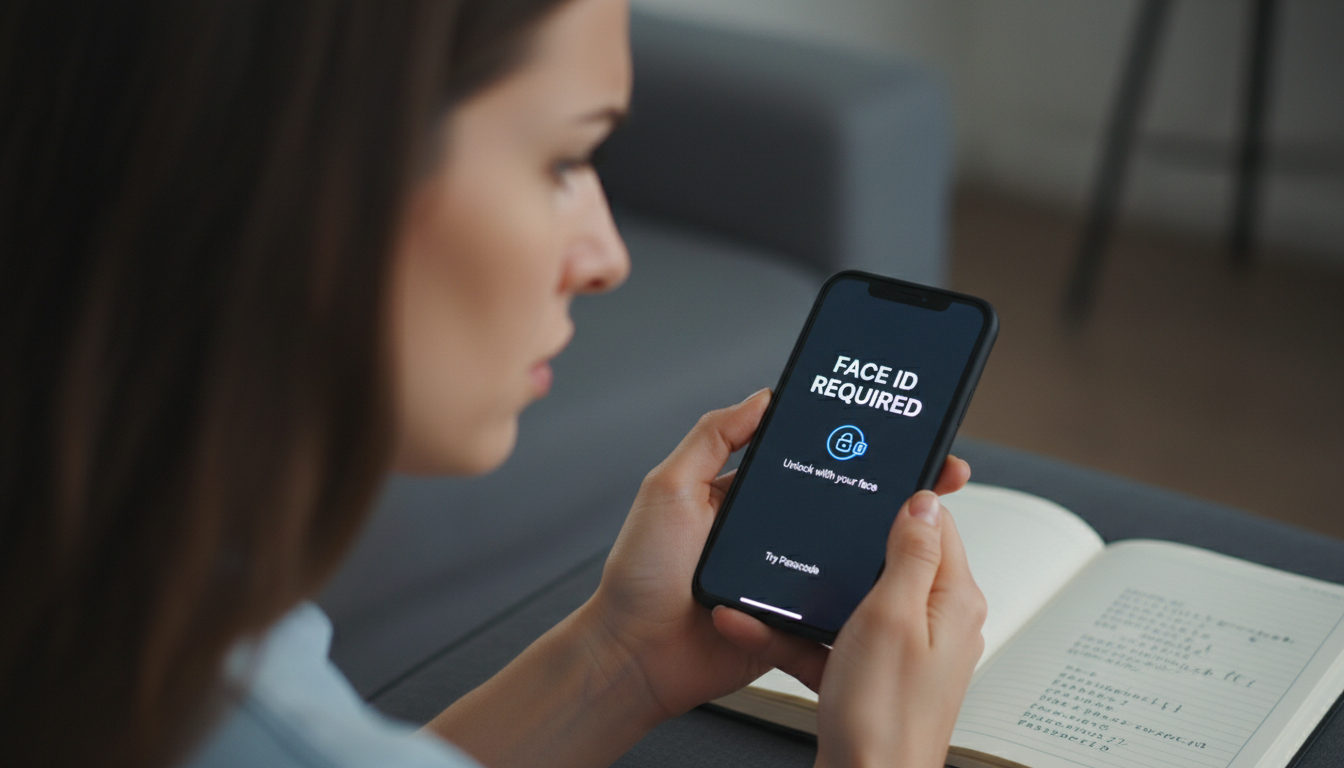

The laptop required Marcus’s fingerprint. Bypassing it required an iCloud recovery phrase. Logging into his primary email to trigger a password reset resulted in a Time-Based One-Time Password (TOTP) request, which was locked inside an authenticator app on his encrypted mobile phone. The physical will, officially stamped and notarized by the state, could not bypass a 256-bit encryption key. Sarah found herself trapped in an endless authentication loop, locked out of the very wealth Marcus spent two decades building for her.

Mistake 1: Believing a Paper Will Reverses Cryptography

The most profound misunderstanding in modern inheritance is the belief that a physical court order commands immediate authority over digital architecture. Historically, a probate judge’s signature forced a bank manager to unlock a physical safe deposit box. Today, technology companies operate under completely different structural parameters.

To bridge this gap, state legislatures adopted the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA). This framework grants executors the legal standing to request access to digital assets. However, legal standing is not the same as technical capability.

"A court order can compel a corporation to release data, but it cannot compel an algorithm to decrypt data if the corporation itself does not possess the encryption keys."

If an account is protected by End-to-End Encryption (E2EE) or Advanced Data Protection, the service provider literally does not have the technical ability to hand over the contents, regardless of what the court document dictates. Relying solely on legal documentation without an automated, cryptographic handover mechanism leaves the estate entirely vulnerable to data loss.

Mistake 2: The "Master Password" Notebook Delusion

For decades, the standard advice for digital estate planning was to write down a master list of passwords and store it in a fireproof safe. In an era of static credentials, this was adequate. Today, it is a fatal point of failure. This common mistakes checklist highlights exactly why physical credentials fail:

- The Session Timeout Risk: Passwords rotate rapidly. A notebook written six months ago inevitably contains outdated credentials for critical financial institutions.

- The Biometric Wall: A physical password accomplishes nothing if the platform challenges the login attempt with a Face ID or Touch ID prompt from a recognized device.

- The SIM-Jacking Threat: Keeping a deceased loved one’s phone line active indefinitely to receive SMS codes exposes the estate to targeted SIM-swap attacks while the estate is in probate.

- The Device Degradation: Hardware fails. Batteries bloat. Relying on a single physical device as a master key guarantees eventual total data loss.

Let us return to Sarah. She found Marcus's secondary notebook hidden in his office drawer. She carefully typed his complex Vanguard password into the login portal. The screen refreshed, demanding a push-notification approval from the primary device. She stared at Marcus's phone resting on the desk, its screen dark, forever locked behind a biometric sensor that could never be activated again. The password was perfectly accurate, and entirely useless.

Mistake 3: Underestimating the Authenticator Trap

Multi-Factor Authentication (MFA) is designed specifically to stop unauthorized access by users who possess a correct password but lack verified context. Ironically, a grieving widow or executor appears to a security algorithm exactly like a hostile foreign hacker. According to the Cybersecurity and Infrastructure Security Agency (CISA), implementing MFA is critical for defending against cyber threats. Yet, estate planners frequently ignore how MFA disrupts lawful inheritance.

Traditional Transfers vs. Digital Authentication Realities

A meaningful comparison between historical inheritance and modern authentication reveals the structural flaw in standard estate planning:

- The Physical Custodian: A traditional executor walks into a bank, presents a death certificate and letters testamentary, and the branch manager legally overrides the account lock to transfer funds.

- The Cryptographic Custodian: An executor attempts to access an online business dashboard. The platform demands a TOTP code generated locally on a dedicated hardware module exactly every 30 seconds. There is no branch manager capable of overriding local hardware verification.

To navigate this, digital estate plans must account for the transfer of the secondary authentication factors themselves, not just the primary passwords. This often means duplicating setup keys or utilizing dedicated legacy systems that securely escrow recovery seeds.

Mistake 4: Failing to Establish Conditional Transfer Mechanics

Leaving an encrypted hard drive with a family member is not estate planning; it is a security vulnerability. If you hand over full access while you are alive, you compromise your immediate operational security. If you hold everything perfectly secret until death, you guarantee the Great Digital Lockout.

The solution requires leveraging conditional logic, specifically a dead man's switch mechanism. This allows an individual to encrypt their most highly sensitive credentials, private keys, and operational blueprints. The system requires rolling check-ins. If the individual goes silent for a pre-determined period—signaling incapacitation or death—the system automatically initiates a secure, time-locked transfer of the decryption keys to verified beneficiaries.

This is exactly why Cipherwill was built. By utilizing zero-knowledge encryption architecture, the actual platform never views your data. Instead, it mathematically enforces your inheritance wishes, automatically bridging the gap between your untimely absence and your family's urgent need for access, entirely independent of slow probate courts.

Mistake 5: Relying Solely on Traditional Estate Attorneys

General practice estate lawyers are brilliant at preventing tax leakage, managing familial disputes, and structuring complex physical trusts. However, as estate lawyers share the biggest digital will mistakes seen across the industry, they are the first to admit they are not cybersecurity engineers.

An executor sitting in a mahogany-paneled law office, staring helplessly at a cold hardware wallet containing millions in unrecoverable digital assets, has become a tragically common scene. The lawyer legally represents the estate, but they cannot code a backdoor into a blockchain.

| Estate Requirement | Traditional Law Firm Approach | Digital Inheritance Platform Approach |

|---|---|---|

| Documenting Intent | Drafts static, physical RUFADAA consent clauses. | Maintains dynamic, encrypted databases updated in real-time. |

| Transfer Execution | Requires multi-month court probate to grant legal authority. | Automates immediate, mathematical key release upon verified absence. |

| Security Against Theft | Stores physical documents in file cabinets vulnerable to fires/loss. | Employs zero-knowledge, quantum-resistant encryption parameters. |

The Secure Family Continuity Checklist

Protecting your legacy requires acknowledging that digital assets behave fundamentally differently than physical real estate. To secure your family’s future, execute this structured continuity framework:

- Inventory the Technical Stack: Document every platform that houses financial value, sentimental data, or business infrastructure, specifically noting which ones rely on biometric locks or hardware keys.

- Implement Redundant Authentication: For critical accounts, configure secondary hardware keys (like a backup YubiKey) and securely store it separately from your primary devices.

- Deploy an Automated Dead Man's Switch: Adopt a zero-knowledge legacy platform to serve as the secure bridge that releases decryption instructions automatically if you fail to check in.

- Update Legal Directives: Ensure your written will explicitly invokes RUFADAA language, granting your designated executor the specialized legal right to handle digital assets.

- Onboard Your Beneficiaries: Have a deliberate, non-technical conversation with your family about the mechanics of legacy access, ensuring they understand the recovery sequence before panic sets in.

Frequently Asked Questions

Question: What exactly is digital estate planning?

Answer: Digital estate planning is the structured process of organizing, securing, and legally transferring your online accounts, digital currencies, digital business assets, and sentimental files to trusted beneficiaries, ensuring they are not permanently locked out by encryption or multi-factor authentication upon your death.

Question: Can my family just reset my passwords after I pass away?

Answer: Generally, no. Without access to your unlocked primary mobile device or biometric data to receive two-step verification codes, families become trapped in authentication loops. Modern security protocols actively block unrecognized login attempts to prevent fraud, effectively locking out your grieving family.

Question: Does a traditional paper will automatically give access to my emails?

Answer: No. While a traditional will might grant legal authority over your estate, technology companies are bound by strict user privacy agreements and end-to-end encryption. A legal document cannot forcefully decrypt a secure device if the technology provider does not possess the encryption keys to begin with.

Question: What is the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA)?

Answer: RUFADAA is a widely adopted legal framework that gives executors, trustees, or power-of-attorney agents the legal standing to request access to your digital assets. However, your explicit prior consent inside a digital legacy platform often legally supersedes the general terms of a basic will under this act.

Question: Why is writing passwords in a notebook considered dangerous?

Answer: Passwords rotate frequently, rendering written lists outdated quickly. More importantly, physical notebooks cannot bypass biometric security locks or local authenticator apps. Falling into the wrong hands while you are still alive also creates an immense, immediate security vulnerability for your identity.

Question: How does a dead man's switch work for digital inheritance?

Answer: A dead man's switch periodically prompts you to confirm you are active. If you fail to verify your presence over a designated timeline—due to incapacitation or death—the secure system automatically triggers the encrypted release of your credentials or recovery instructions directly to your predefined beneficiaries.

Question: What happens to unmanaged cryptocurrency when someone dies?

Answer: If an individual holds digital currency in self-custody wallets and dies without securely transferring the recovery seed phrases, those funds are mathematically lost forever. No court order, legal mandate, or state intervention can recover assets secured on a blockchain without the corresponding private key.

Question: How is zero-knowledge encryption used in estate platforms?

Answer: Zero-knowledge architecture ensures that the platform storing your digital will encrypts your data locally on your device. The provider mathematically cannot read, scan, or exploit your passwords or instructions. Only your designed beneficiaries obtain the necessary cryptographic keys to decrypt the information when the time comes.

By Cipherwill Editorial Team, Reviewed by Cipherwill Review Board, Trust & Security Review Team

Editorial contributor: Iraan Qureshi

Review contributor: Reyansh Mehta