Estate planning often conjures images of complex legal documents and daunting decisions. However, understanding the various tools available can simplify the process and provide immense peace of mind. One such powerful tool is a particular type of trust, which offers significant advantages over a traditional will in many situations, primarily due to its flexibility and privacy. This instrument allows for the seamless transfer of assets and can be a cornerstone of a well-structured financial future.

This specific trust is established during your lifetime, giving you full control over your assets while you are alive and capable. You can modify, amend, or even revoke it entirely, hence its namesake. This adaptability is a key feature, distinguishing it from irrevocable trusts where changes are far more difficult to implement once established. It acts as a private contract, dictating how your property will be managed and distributed.

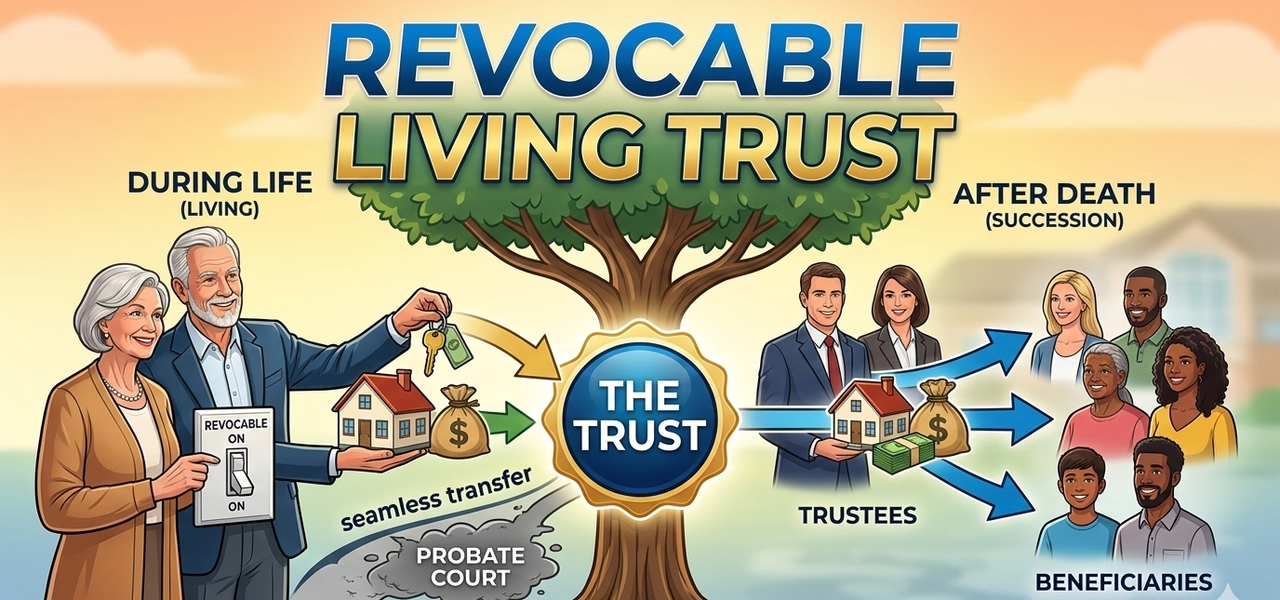

Understanding the Core Mechanism

At its heart, this trust involves three key roles: the grantor (you, who creates the trust), the trustee (who manages the assets within the trust), and the beneficiaries (who ultimately receive the assets). Often, the grantor initially serves as both the grantor and the trustee, maintaining complete control. This arrangement ensures that your financial life continues without interruption.

Upon your incapacitation or death, a successor trustee, whom you've designated, steps in to manage or distribute the assets according to your precise instructions. This smooth transition is a primary benefit, avoiding the delays and public nature of probate court. The assets held in the trust are legally owned by the trust itself, not by you personally, which is crucial for its operational advantages.

The Probate Avoidance Advantage

One of the most compelling reasons individuals choose this trust is to bypass the probate process. Probate is the legal procedure through which a will is validated and an estate is settled, often involving court fees, attorney fees, and a considerable amount of time. Depending on the state, this process can stretch for months or even years, delaying beneficiaries' access to their inheritance.

By transferring your assets into this trust, they are no longer part of your personal estate subject to probate. Instead, they are distributed privately and efficiently by your chosen successor trustee, adhering to the terms you established. This saves your loved ones time, money, and the emotional burden of navigating the court system during an already difficult period.

Maintaining Privacy and Control

Unlike a will, which becomes a public document once submitted to probate, the terms of this trust remain private. This confidentiality can be invaluable for families who wish to keep their financial affairs out of the public eye. It also allows for more discreet and nuanced distribution plans, especially in complex family situations.

Furthermore, you retain complete control over your assets throughout your lifetime. You can buy, sell, or manage property held within the trust just as you would if it were in your personal name. The trust simply acts as a holding mechanism, providing a framework for future management and distribution without surrendering your present authority.

Managing Incapacity Gracefully

Beyond death, the trust provides a robust plan for managing your assets should you become incapacitated. Without such a document, a court might need to appoint a conservator or guardian to manage your finances, a process that can be costly, time-consuming, and potentially involve someone you wouldn't have chosen.

With this trust, you explicitly name a successor trustee who can immediately step in and manage your affairs according to your wishes, without court intervention. This ensures that your bills are paid, investments are managed, and your care is provided for, all under the guidance of someone you trust. It's a proactive measure that safeguards your well-being.

When Is It the Right Tool?

This estate planning tool is particularly beneficial for individuals with significant assets, those who own real estate in multiple states, or anyone desiring to avoid probate. It's also ideal for those with complex family dynamics, such as blended families, where specific distribution instructions are critical to prevent disputes.

If you have minor children or beneficiaries with special needs, this trust can establish protective sub-trusts to manage their inheritance responsibly over time. It offers a level of control and customization that a simple will cannot match. For many, it truly forms the backbone of a comprehensive estate plan.

Setting Up the Trust: Key Steps

Establishing this trust involves several crucial steps. First, you draft the trust document with the help of an attorney, outlining your wishes for asset management and distribution. This document names your initial trustee, successor trustees, and beneficiaries.

Second, and critically, you must "fund" the trust by transferring ownership of your assets into the trust's name. This means retitling real estate, changing beneficiary designations on financial accounts, and assigning personal property. An unfunded trust, while legally valid, cannot achieve its intended purpose of probate avoidance.

Funding the Trust: Best Practices

Proper funding is paramount. Assets that are not formally transferred into the trust will still be subject to probate. It's essential to work with your attorney to ensure all intended assets are correctly retitled. This includes bank accounts, investment portfolios, real estate, and often valuable personal property.

Some assets, like IRAs and 401(k)s, have specific rules regarding trust ownership and beneficiary designations. It's important to understand these nuances to avoid unintended tax consequences. Regularly reviewing and updating your trust and asset titles is also a best practice, especially after major life events.

Potential Risks and How to Mitigate Them

While highly advantageous, there are some potential downsides. The initial setup cost is generally higher than drafting a simple will. Additionally, the administrative burden of funding the trust and maintaining accurate records falls on the grantor. Forgetting to fund assets can undermine the trust's effectiveness.

To mitigate these risks, choose an experienced estate planning attorney who can guide you through the process. Maintain clear records of all assets transferred. Regularly review your trust document and asset titles, perhaps annually or bi-annually, to ensure they align with your current wishes and holdings.

The Digital Estate Dimension

In today's interconnected world, an often-overlooked aspect of estate planning is the digital estate. This includes online accounts, digital assets, and virtual currencies. Traditional estate planning documents, including this trust, may not adequately address the complexities of managing and distributing these assets.

This oversight can lead to significant challenges for your loved ones trying to access or close online accounts. Think about your social media profiles, email accounts, cloud storage, and cryptocurrency holdings. Without clear instructions and access, these digital footprints can become inaccessible or remain in limbo indefinitely. For a deeper dive into this critical area, you might find valuable insights in this Cipherwill blog post: Why Procrastination is the Biggest Threat to Your Digital Estate.

Integrating Digital Estate Solutions

The challenge of managing digital assets effectively alongside a traditional trust can be daunting. Many individuals struggle with organizing passwords, account information, and specific instructions for their digital presence. This is where comprehensive solutions designed for the digital age become indispensable.

For individuals seeking a streamlined approach to managing their digital legacy and ensuring their digital assets are handled according to their wishes, Cipherwill offers an innovative and secure solution. It bridges the gap between traditional estate planning and the digital world, providing a centralized platform to organize, store, and securely transmit critical digital information to your designated beneficiaries or executors. Cipherwill acts as your trusted partner, ensuring your digital footprint is managed with the same care as your physical assets, making it a crucial component for any forward-thinking estate plan.

Real-World Applications and Examples

Consider a couple who owns a vacation home in a different state from their primary residence. If they only have a will, their beneficiaries would have to go through probate in both states, a process known as ancillary probate. By placing both properties into this trust, they completely circumvent both probate processes, saving significant time and money.

Another example is a single parent with a child who has special needs. Through this trust, they can establish a special needs trust as a sub-trust, ensuring that the child's inheritance is managed by a professional trustee without jeopardizing their eligibility for government benefits. This provides long-term financial security and peace of mind.

Ongoing Management and Review

Establishing this trust is not a one-time event; it's an ongoing process. Life changes – marriages, divorces, births, deaths, changes in assets, or changes in laws – all necessitate a review of your trust document. It's advisable to revisit your trust every few years or after any significant life event.

Regular review ensures that your trust continues to reflect your wishes and remains effective. Working with your estate planning attorney to make necessary amendments will prevent outdated provisions from creating complications in the future. This proactive approach guarantees your plan remains robust and relevant.

---

Frequently Asked Questions

Q: What is the main difference between this trust and a will?

A: The primary difference is that this trust avoids probate because assets are owned by the trust, not you personally, while a will must go through probate to distribute assets. This trust also offers privacy and can manage assets during incapacitation.

Q: Can I put all my assets into this type of trust?

A: Most assets, including real estate, bank accounts, investment accounts, and personal property, can be transferred into this trust. However, specific assets like IRAs and 401(k)s require careful consideration of beneficiary designations to avoid tax penalties.

Q: Do I lose control of my assets once they are in the trust?

A: No, you do not. As the grantor and often the initial trustee, you retain complete control over all assets placed in this trust. You can buy, sell, manage, or transfer assets as you wish, and you can amend or revoke the trust at any time.

Q: Is this type of trust expensive to set up?

A: Generally, the initial cost of setting up this trust is higher than drafting a simple will due to its complexity and the need for asset transfers. However, it can save significant money in probate fees and legal costs in the long run.

Q: What happens if I become incapacitated and have this trust?

A: If you become incapacitated, the successor trustee you named in the trust document will step in to manage your assets according to your instructions, without the need for court intervention, such as a conservatorship or guardianship.

Q: Can I change my beneficiaries or other terms of the trust?

A: Yes, absolutely. This trust is "revocable," meaning you can modify, amend, or completely revoke it at any point during your lifetime, as long as you are mentally competent. This flexibility is one of its key advantages.

Q: What is "funding" the trust, and why is it important?

A: Funding the trust means legally transferring ownership of your assets from your personal name into the name of the trust. It is crucial because an unfunded trust will not avoid probate for those assets, defeating one of its main purposes.

Q: Does this trust protect assets from creditors?

A: Generally, no. Because you retain full control over the assets in this trust, they are typically not protected from your creditors during your lifetime. Asset protection is usually achieved through irrevocable trusts or other legal strategies.

Q: Do I still need a will if I have this trust?

A: Yes, it's highly recommended to have a "pour-over will" alongside this trust. This will acts as a safety net, ensuring any assets not formally transferred into the trust during your lifetime are "poured over" into the trust upon your death, to be distributed according to its terms.

Q: How often should I review and update my trust?

A: You should review your trust document every three to five years, or after any significant life event, such as marriage, divorce, birth of a child, death of a beneficiary or trustee, significant change in assets, or changes in estate tax laws.