When leaving money to a neurodivergent child or adult beneficiary, standard wills are fundamentally broken. They assume the heir possesses the exact type of executive function required to navigate a hostile labyrinth of probate courts, medallion signature guarantees, and high-stakes banking deadlines. For individuals living with ADHD, Autism, or other cognitive variations, this sudden administrative burden can trigger debilitating operational paralysis, leading directly to lost assets or unwittingly compromised government health benefits. To ensure a truly safe financial transition, parents must move beyond traditional, paper-heavy legal frameworks. It is essential to build an easy inheritance system—utilizing streamlined digital vaults, exploring accessible special needs trust alternatives, and providing intuitive, low-friction access to generational wealth rather than handing over a chaotic legal puzzle to a brain built for different workflows.

The Myth of the Airtight Document: Why Standard Wills Fail Neurodivergent Minds

The most pervasive myth in traditional generational wealth transfer is that a legally valid document is the only thing needed to secure a child's future. Parents spend thousands of dollars drafting immaculate paperwork under the assumption that money inherently solves problems. But for an autistic adult or an ADHD beneficiary, a sudden inheritance is not just a financial windfall; it is a sprawling, high-stakes project management assignment dumped on them during the peak of acute grief.

General probate systems and inheritance workflows act like PC software violently forced onto a Mac operating system. The traditional estate liquidation process operates on strict, unforgiving timelines governed by the Uniform Probate Code and various state statutes. Courts demand multi-step, sequential planning. Banks require persistent phonetracking and wet-ink identity verification. These are the exact environments where executive dysfunction—struggles with task initiation, working memory, and sustained attention on non-preferred tasks—creates a massive vulnerability.

"You aren't just leaving your child wealth; without a streamlined system, you are leaving them a bureaucratic second job that their brain is fundamentally not equipped to perform."

To properly construct an estate plan for autistic adults or an ADHD beneficiary guide that actually works, planners must bridge the gap between legal theory and operational reality. The goal is no longer just identifying who gets what, but fundamentally engineering how they receive it.

A Tale of Two Systems: Meeting Marcus

Consider the reality of Marcus, a 28-year-old software engineer living with combination-type ADHD and mild support needs on the autism spectrum. When his mother unexpectedly passed away, she left behind a traditional, legally pristine 40-page Last Will and Testament naming Marcus as the primary executor and beneficiary. She assumed she had protected him.

Instead, Scene One unfolds in an overwhelming law office. Marcus is handed a dense stack of heavily watermarked paper. The lawyer casually instructs him to "obtain Letters Testamentary, call the three different brokerages, freeze the utility accounts, and secure a Medallion Signature Guarantee for the mutual funds." For someone whose executive function fluctuates daily—managing a full-time job while barely remembering to renew his car registration—this verbal list of vague, multi-step institutional tasks sounded like speaking a foreign language backward.

The result was not proactive management, but profound avoidant paralysis. Envelopes piled up for six months. A crucial life insurance policy nearly lapsed due to unreturned claim forms, and the sheer mental weight of uncompleted tasks plunged Marcus into severe autistic burnout. The money was technically his, but operationally trapped behind an invisible wall of administrative hostility.

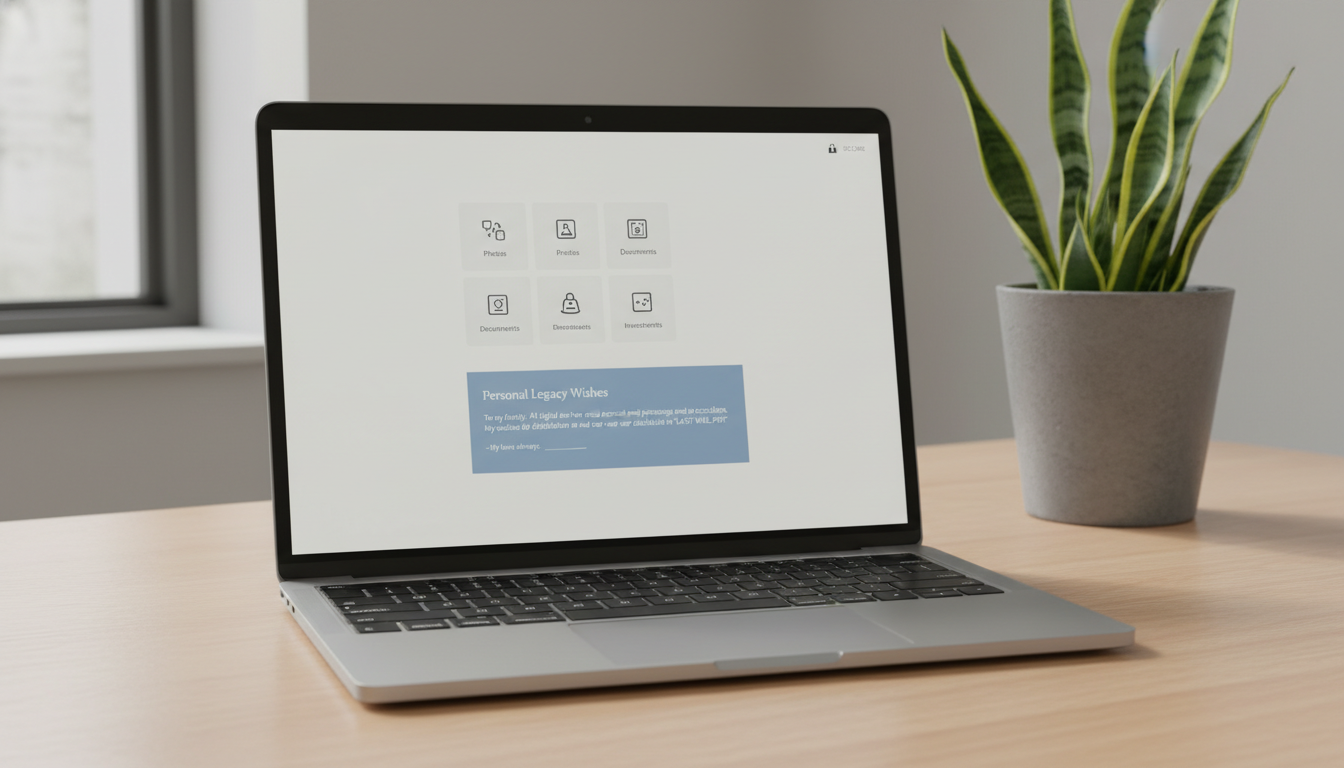

Contrast this with a neuro-inclusive infrastructure. Scene Two: Marcus logs into a secure internet portal his mother set up beforehand. He doesn't have to guess where her bank accounts are; they are visually mapped out on a digital dashboard. He doesn't have to hunt for the life insurance policy number; it is clearly displayed alongside step-by-step, plain-language instructions on who to call and what exact script to read. Her digital legacy system inherently accommodated his need for structure, turning an insurmountable mountain of administrative terror into a series of achievable, low-friction clicks.

Protecting the Baseline: Benefits, Trusts, and the $2,000 Cliff

Administrative burnout is only one half of the danger; the other half is the catastrophic loss of structural support. Many neurodivergent individuals, specifically those with higher support needs, rely on state and federal assistance. The Social Security Administration enforces a strict $2,000 resource limit for Supplemental Security Income (SSI) eligibility. If a well-meaning parent leaves a standard $50,000 liquid inheritance directly to their child, it instantly breaches this ceiling, triggering an immediate severance of SSI and, consequently, Medicaid.

To prevent this devastating cliff, families historically relied exclusively on Third-Party Special Needs Trusts (SNTs). While legally sound, SNTs are operationally rigid. A corporate trustee acts as a gatekeeper, requiring the beneficiary to submit receipts and formal requests for everyday purchases. For a beneficiary suffering from severe executive dysfunction, navigating a stubborn, slow-moving corporate trustee just to buy sensory tools or fund a specialized therapist causes highly unnecessary friction.

Exploring Special Needs Trust Alternatives

Modern estate planning for autistic adults demands flexibility. While an SNT might hold heavy real estate, liquid day-to-day funds are increasingly managed through ABLE Accounts. Established by the Stephen Beck Jr., Achieving a Better Life Experience Act of 2014, these tax-advantaged savings accounts allow individuals whose disability onset occurred before a specific age to save substantial funds (often up to $100,000) without threatening their SSI eligibility. More importantly, ABLE accounts are often equipped with standard debit cards, empowering the beneficiary with direct, frictionless purchasing power without begging a trustee for permission.

Meaningful Comparison: Structuring the Wealth Transfer

When determining how to allocate the physical and digital inheritance, weighing the operational demands of each vessel is paramount. The following comparison highlights how different legal infrastructures demand different levels of executive function from the heir.

| Inheritance Mechanism | Execution Friction for Neurodivergent Heirs |

|---|---|

| Direct Inheritance (Standard Will) | Extremely High. Requires court appearances, dense paperwork, managing probate deadlines, and places government benefits at severe risk if asset limits are breached. |

| Special Needs Trust (Discretionary) | Moderate to High. While legally protective, it often requires high executive function to manage communications with a strict corporate trustee and track disbursement receipts. |

| ABLE Account Funding | Low. Protects SSI/Medicaid benefits while offering direct debit-card access for approved disability expenses, bypassing bureaucratic gatekeepers entirely. |

| Digital Vault Transfer (e.g., Cipherwill) | Virtually Zero. Provides a secure, automated, and pre-organized map of all accounts, credentials, and step-by-step instructional contexts directly to the trusted beneficiary. |

Ultimately, the most resilient plans rarely rely on just one mechanism. A family might use an SNT to hold the family home and dividing a residuary estate safely, an ABLE account for daily operational liquidity, and a digital vault to seamlessly connect the beneficiary to the instructions and credentials necessary to activate both.

The Administrative Panic Threshold: Overlooked Procedural Risks

When mapping out an easy inheritance system, you must identify where the "Administrative Panic Threshold" lies for your specific child. These are the highly specific, deeply tedious institutional friction points that frequently cause an ADHD or Autistic beneficiary to abandon the process entirely.

- The Medallion Signature Guarantee Nightmare: Transferring legacy stock certificates or changing ownership of major brokerage accounts often requires a Medallion Signature Guarantee, regulated by U.S. Securities and Exchange Commission (SEC) enforcement standards. This requires the beneficiary to travel physically to a specific bank branch, prove their identity, and bring original death certificates—a brutal sequential task for someone combating sensory and operational overload.

- Multi-Factor Authentication (MFA) Lockouts: If your assets are secured by your personal phone number, your death effectively bricks the accounts. If your child cannot unlock your specific MFA device, they cannot consolidate the assets, regardless of what the physical will dictates.

- Cryptocurrency Wallet Attrition: Physical wills do not securely transmit private crypto keys or seed phrases. A neurodivergent heir faced with piecing together scattered hardware wallet instructions will likely abandon the asset entirely to avoid the unmanageable stress.

- Probate Bonding Requirements: In many jurisdictions, if the will doesn't explicitly waive it, the executor must qualify for a surety bond. Getting approved for a bond requires passing credit checks and navigating tedious insurance paperwork—a massive roadblock for a young adult with limited financial history.

Building an Easy Inheritance System: A Practical Execution Framework

Moving from a broken, paper-heavy legal model to a functional, highly operational asset transfer requires intentional engineering. Use this structured decision framework to organize your legacy in a way that respects how a neurodivergent mind processes information.

- Consolidate the Institutional Footprint: Before you focus on documents, minimize the moving parts. If you have five different checking accounts, consolidate them into one. If you have trailing 401(k)s from old jobs, roll them into a single IRA. You are reducing the number of phone calls and identity verification steps your child will eventually have to execute.

- Map the Legacy in a Centralized Digital Vault: Standard legal documents tell the court what should happen; a digital vault tells your child exactly how to make it happen. By utilizing a secure digital legacy inheritance platform, you can securely store account locations, subscription cancellations, digital keys, and necessary contacts all in one encrypted environment. Once legally activated, it automatically delivers a highly organized dashboard rather than a scavenger hunt.

- Draft a Contextual "Letter of Instruction": A legal will is incredibly dense. Write a supplementary, plain-language document. Use bold headings, short bullet points, and exact phone numbers. Explain where the physical keys to the house are, what the pin code to the alarm is, and who to call for help with the taxes. Strip out the legalese and write it exactly how you would speak to them on a Tuesday afternoon.

- Appoint a Supportive Co-Pilot: If your child is highly likely to succumb to task paralysis, formally pair them with an administrative ally. This could be a neurotypical sibling, a trusted aunt, or a professional fiduciary. Name this person as a co-executor or legacy contact so the neurodivergent heir doesn't have to bear the full weight of bureaucratic calls alone.

- Automate Immediate Liquidity: Utilize Transfer-on-Death (TOD) or Payable-on-Death (POD) designations on a specific, targeted checking account that can quickly funnel into their ABLE account or a trust. These designations bypass the massive delays of standard probate, ensuring they have the cash to pay immediate bills while the broader estate is processed.

Common Mistakes Parents Make When Planning

Even the most loving and well-intentioned parents frequently stumble into procedural traps that inadvertently harm their autistic or ADHD beneficiaries. Avoid these critical errors:

- Relying exclusively on the legal system: Believing that signing a Will is the final step, completely ignoring the mechanical difficulty of transferring digital assets and closing out modern web-based subscriptions.

- Failing to update Special Needs Trusts: Setting up a blind trust twenty years ago and never reviewing it to see if simpler tools, like modern ABLE accounts, could provide the same protection with vastly more dignity and autonomy.

- Hiding the plan from the beneficiary: Assuming that shielding the child from the stress of estate planning is protective. Springing a massive financial operational shift on a neurodivergent adult post-trauma is disastrous; they need time to familiarize themselves with the platforms and expectations in advance.

- Naming rigid institutional trustees: Appointing a massive bank to oversee a discretionary trust for a child who struggles deeply with formal communication, practically ensuring the child will never ask for the money they need due to social friction.

- Leaving equal but unequal burdens: Leaving 50% of the estate to an ADHD child and 50% to a neurotypical child without acknowledging that the administrative burden of claiming that 50% is exponentially heavier for the ADHD sibling.

Closing the Empathy Gap in Estate Planning

Leaving money to a neurodivergent child is not simply a matter of arithmetic. It is an act of profound operational empathy. The traditional probate system is inherently unyielding, demanding a level of bureaucratic stamina that is actively hostile to neurodivergent minds. Recognizing this vulnerability is the first step toward true legacy protection.

By dismantling complex legal puzzles and replacing them with intuitive, digital-first workflows, visual dashboards, and automated protections, you remove the hidden tax of executive dysfunction from your inheritance. A well-designed estate plan shouldn't just technically fund your child's future; it should seamlessly integrate into the way they actually live, process, and thrive in the world, allowing them to grieve with peace instead of paperwork.

Frequently Asked Questions

Question: Why is leaving money directly to an autistic adult often considered dangerous?

Answer: Leaving money directly can immediately disqualify the beneficiary from crucial government support programs like SSI and Medicaid due to strict resource limits. Furthermore, the administrative burden of managing a sudden liquid windfall can overwhelm their executive function, leading to acute financial mismanagement and deep anxiety.

Question: What happens to an ADHD beneficiary when they are named as a sole executor?

Answer: While entirely legally permissible, placing an ADHD beneficiary as sole executor often results in severe task paralysis. Navigating strict probate deadlines, making endless phone calls to banks, and processing dense legal forms conflicts directly with common executive dysfunction traits, stalling the estate transfer significantly.

Question: How does an ABLE account differ from a standard checking account for inheritance?

Answer: An ABLE account is a specialized tax-advantaged savings mechanism that permits individuals with qualifying disabilities to save beyond standard thresholds without jeopardizing SSI or Medicaid eligibility. Unlike a standard account, the funds within an ABLE account are shielded from federal benefit asset testing up to state-specific limits.

Question: Should I avoid using Special Needs Trusts entirely?

Answer: No, Special Needs Trusts remain highly robust tools for holding large assets, real estate, or substantial generational wealth. However, they should be thoughtfully combined with more accessible tools, like ABLE accounts and clear digital inheritance systems, to prevent forcing the beneficiary to battle a trustee for minor daily expenses.

Question: How does digital asset mapping help neurodivergent heirs?

Answer: Digital mapping replaces a terrifying scavenger hunt with a visually structured dashboard. Instead of deciphering vague paperwork, neurodivergent heirs are provided direct links, plain-text login procedures, and automated step-by-step instructions, completely bypassing the extreme working memory demands of traditional estate settling.

Question: What are Medallion Signature Guarantees and why do they cause friction?

Answer: Governed by strict financial regulations, a Medallion Signature Guarantee is a rigorous in-person security verification required to transfer certain major securities. It demands physical travel, original documentation, and real-time social navigation, which heavily exacerbates sensory and operational overload for certain disabilities during a bereavement period.

Question: Can I leave step-by-step videos alongside my legal will?

Answer: Absolutely. While a video does not legally replace a signed will or replace court mandates, utilizing a secure digital vault to store supplementary instructional videos or audio recordings provides incredibly comforting, accessible guidance for beneficiaries who process visual or auditory information better than dense text.

Question: How do I ensure my digital subscriptions don’t overwhelm my child?

Answer: The strongest proactive step is consolidating your physical footprint and entering all ongoing subscriptions, utilities, and auto-pay accounts into a digital inheritance platform like Cipherwill long before passing. Providing a concrete, explicit cancellation checklist prevents the heir from enduring endless hours on support hotlines.

By Cipherwill Editorial Team, Reviewed by Cipherwill Review Board, Trust & Security Review Team

Editorial contributor: Samarjeet Vohra

Review contributor: Ishani Debroy

Disclaimer: The content provided in this article is for educational and informational purposes only and does not constitute medical, psychological, legal, financial, or tax advice. Standard practices may vary wildly based on an individual's specific diagnosis or regional jurisdiction. Please consult with qualified specialists and attorneys regarding your trust structuring and wealth transfer needs.